Introduction

The Insurance Distribution Directive1 (IDD) was introduced just over five years ago as a broad-ranging requirement for insurance manufacturers and distributors to consider how products were made, advised on and sold.

Although the directive focuses on distribution, it also contains requirements around product oversight and governance (POG) for manufacturers.

Over the last few years, the European Insurance and Occupational Pensions Authority (EIOPA) has become increasingly active in one area of POG—addressing perceived shortcomings in the Value for Money (VfM) of insurance products, particularly in the unit-linked market. In this note, we look at POG through a VfM lens and explore how key concepts introduced by IDD flow through all aspects of product-related conduct risk.

Since the original Directive and supporting Delegated Regulations were brought into force, IDD was extended in 20212 to bring integration of sustainability factors, risks, and preferences into POG, conduct of business and investment advice rules.

Although IDD introduced some key concepts, which provide an underpinning for considering VfM, EIOPA also recognised a lack of clear benchmarks and methodologies for supervising VfM in the European unit-linked market under the POG framework, which has hindered effective application.

Value for Money

Introduction and development

From 2021, EIOPA started the “heavy lifting” of considering a supervision framework for VfM, particularly in relation to unit-linked products. Various pieces of work by EIOPA, including thematic reviews and the annual Cost and Past Performance reports,3 indicated that costs for unit-linked products were high in several European markets and this was having a detrimental impact on customer returns.

Their initial consultation in 20214 proposed a short definition of VfM, bringing in key concepts from IDD and framing the definition in relation to proportionality of costs to benefits and in comparison to other retail products in the market in which the product operates.

The consultation proposed four key principles for VfM:

- Costs and charges needed to be due, i.e. they correspond to a specific service offer which responds to a target market need.

- VfM should be assessed at both the product level and the product feature/option level, which in the context of unit-linked products means at the individual fund choice within a product’s range.

- VfM needed to be reviewed regularly through the product lifetime.

- Products should be easily understood by all stakeholders.

The consultation was followed up by a 2021 Supervisory Statement,5 which built upon the above principles to develop a framework and common approach across supervisors for addressing VfM risk. The Statement unsurprisingly indicated that VfM assessment should be done and evidenced by structured and documented processes by insurers.

With the scene set, EIOPA moved on in 2022 to set out a VfM assessment methodology for supervisors.6 The aim of this methodology was to enable supervisors to drill down through markets and providers to individual products, coming to a conclusive decision as to whether they offered VfM to their identified target market.

The assessment methodology is also useful to insurers in that it sets out a series of illustrative quantitative indicators that could be used to assess VfM, including measures for investment products assessed at a variety of policy durations such as:

- Surrender value vs. premium paid

- Total costs vs. premium paid

- Reduction in yield (RIY)

- Net real return (net of inflation) per annum

It also proposed similar indicators for products with biometric risk benefits.

This second phase of VfM supervision development has continued with EIOPA’s 2024 consultation on Methodology for VfM Benchmarks.7 This consultation proposes taking the indicators described in the methodology above, applying them to the data collected under the annual EIOPA Cost and Past Performance Report, and thereby determining VfM benchmarks for different homogeneous product clusters.

Key VfM learning points from IDD concepts

A number of key ideas flow through IDD and, more recently, we can see their incorporation into the VfM work done by EIOPA. These key ideas include:

- Identifying the target market customers for insurance products at a suitably granular level, determined by the product complexity. This includes analysing their needs, objectives, interests and characteristics.

- Product testing is conducted before products are brought to market to ensure they meet the needs of the target market customers and are understood by them.

- Product reviews are conducted at regular intervals—looking back at products throughout their lifecycle to ensure they continue to meet the needs of the target market customer.

- Distribution governance—Is the distribution channel still suitable for the target market customers, and is there a good two-way flow of information on products and customers between the insurer and distributor?

Without insurers having these building blocks in place, it makes POG in general and VfM in specific very difficult to manage.

IDD & VfM POG checklist

From our work with clients, we have identified a number of key characteristics of good quality POG and VfM documentation. Most insurers will have at least some of these in place already, but this provides a useful checklist for an assessment of an operational POG documentation and controls suite:

Figure 1: POG & VfM checklist

☑ A target market definition for products and product features/options, with appropriate granularity w/r/t product complexity. |

☑ Product design process and documentation addressing implications of this complexity. |

Pricing process and documentation covering: |

|

☑ Properly identifying and quantifying due costs and charges. |

|

☑ The relationship to target market customer needs, objectives and characteristics. |

|

☑ Identification, quantification and linking costs/charges and benefits over a range of scenarios. |

|

☑ Comparison to market standards and the competitive landscape. |

|

☑ Costs at a fund level, especially for “own brand” funds. |

|

☑ Controls to ensure conflicts of interest are managed and mitigated. |

☑ A clearly signposted process to assess VfM within the POG policy. |

☑ Comprehensive quantitative and qualitative VfM testing across holding periods and product features/options. |

☑ Product review triggers (regular and ad-hoc), processes and documentation, covering VfM, costs and charges, performance, guarantees, coverage and services, and fund performance reviews. |

☑ Adequate systems and controls to minimise the risk of products being mis-sold. |

Developing VfM policy

For those at the beginning of the VfM journey, the challenge of starting with a blank piece of paper isn’t to be underestimated, and early decisions made at this stage of the process can influence the usefulness of the VfM policy, for better or for worse.

For example, basing a VfM assessment process on the EIOPA Level I/II/III assessment methodology sounds useful. But this methodology is designed as a filtering process for supervisors to drill down from the overall market to products they wish to investigate further. To be effective, a company policy must be based on a more comprehensive approach, which requires the same level of scrutiny across all its products.

Another area of difficulty is what EIOPA is calling Multi-Option Products (MOPs). This describes products with a range of investment fund options, i.e. the norm in the Irish/UK and EU cross-border market. EIOPA’s approach is driving towards considering each fund option as a separate sub-product and applying VfM to them individually. This approach can pose problems, for example in looking at long-term returns of cash or deposit funds, which are likely to be very low or even negative during periods of low interest rates, taking into account product charges.

Product providers, particularly in the cross-border market, try to differentiate themselves not only from other cross-border providers but also from domestic insurers. However, differentiation tends not to come cheap, so consideration and documentation of the qualitative product elements is important. EIOPA provides some pointers here, specifically mentioning:

- Product sustainability features

- Digitalisation of customer interaction

- Customised advisory/assistance – initial or ongoing

- Non-monetary bonuses or more generous risk exclusions

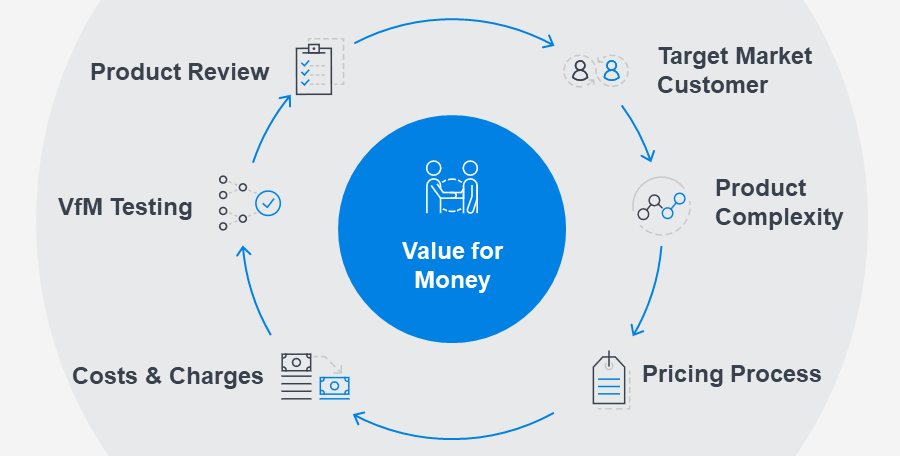

The VfM product cycle

The ideal VfM policy is one that can be used to inform decisions at multiple stages of the product cycle.

Figure 2: The product cycle

For new products, VfM consideration should be part of the pricing process—looking at the design of charging structures, and identification of costs and charges—in order to deliver a product that meets the target market customer needs.

During the product testing process, determining whether the product meets or fails the VfM testing criteria is fundamental. However it also has a prominent place in target market customer testing of the product.

Finally, VfM considerations, particularly in relation to past fund performance and actual customer financial outcomes, are important for the product review process under POG.

Learnings on VfM policyIn constructing a VfM policy, EIOPA’s assessment methodology, as summarised above, is a tool primarily aimed at supervisors but can also be used to inform the key areas needed for a VfM policy.

Insurers’ VfM policies need to be specified in enough breadth to apply appropriate measures to different product types, e.g. unit-linked savings/accumulation, non-linked protection, unit-linked decumulation, with profits.

Also, the policy needs to be considered at a number of points in the proposition cycle, e.g. during the initial conceptual phase, detailed development and pricing, testing and finally during in-force product reviews.

The tried and tested Red/Amber/Green (RAG) assessment approach linked to specific quantitative hurdle rates consistent with product type is hard to beat. This can be applied to the full range of metrics mentioned in the methodology, e.g. RIY at the product’s Recommended Holding Period (RHP) and intermediate periods, biometric costs, cost/premium ratios, etc.

However, these RAG assessments need to be grounded in the real world of economic factors and customer needs. Calibration to these needs and the competitive marketplace is essential.

For funds, a process for reviewing fund performance versus. benchmark and versus peers is critical element of VfM. This may be present in the insurers’ investment governance and oversight function, but it should also be integrated into POG and VfM in order to assess actual customer outcomes as opposed to the theoretical outcomes implied by assumed future growth rates.

For now, insurers should be prepared to look at product performance under various growth scenarios (PRIIPS methodology is a good start here as EIOPA have flagged in the Benchmarking consultation in relation to internal rate of return (IRR) calculations). But as VfM evaluation becomes more visible, they should be prepared to develop stochastic analysis in the future.

Finally, the regulatory focus for now is likely to be on products which are open to new business, but insurers should be prepared to consider VfM on closed products in the future.

VfM and product aims

When it comes to products that are likely to pass VfM assessments, here are some rules of thumb to consider:

- Avoiding the “tail” of RIY or fund past performance metrics (relative to or versus the benchmark) in the universe of target market products is advisable. However insurers can potentially offset the implicit poor VfM of low rankings in these areas through novel product features or other qualitative “added value” that can be documented and justified.

- Product cost indicators should be “as low as possible” (per EIOPA’s assessment methodology), but with some proportionality depending on the underlying investment strategy.

- Break-even IRRs should be “as low as possible” to ensure resilience in adverse market development.

- Any biometric risk benefits should be greater than the premium paid, at the RHP—and “the higher the better."

- Novel or differentiating features of the product should be highlighted in POG documentation for their potential VfM impact.

How Milliman can help

Value for Money of the typical unit-linked products sold in western European markets is an emerging and evolving topic, and one which is attracting increasing levels of regulatory scrutiny.

The latest step in this process is EIOPA’s 2024 consultation on Methodology for VfM Benchmarks, which will likely lead to usage of these benchmarks by supervisors to assess products in their marketplace late in 2024 or 2025.

Milliman has helped a number of insurance clients with developing or reviewing a VfM policy as part of their overall POG framework through the following processes:

“Fast start” workshops on VfM issues, covering

- Regulatory guidance

- Company business model and product range

- Target market

- Competitive landscape

Incorporating VfM policy into the POG framework

- Extending and expanding the policies on pricing and profitability and regular product review

Review of developed VfM policies

- Metrics or hurdle rates

- Qualitative assessment

- Emerging best practice

Market surveys

- Quantitative metrics

- Questions on policy or process

Regulatory liaison

- Regulatory communications

- Assisting with specific queries or responses to e.g. thematic reviews

From our work in these areas, we believe we have a wide range of experience that we can bring to bear to benefit your business.

1 https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32016L0097.

2 https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32021R1257.

3 https://www.eiopa.europa.eu/system/files/2023-01/costs_and_past_performance_report_2023_0.pdf.

4 https://www.eiopa.europa.eu/system/files/2021-04/consultation-paper-framework-to-address-value-for-money.pdf.

5 https://www.eiopa.europa.eu/system/files/2021-11/supervisory_statement_on_assessing_value_for_money_in_the_unit-linked_market.pdf.

6 https://www.eiopa.europa.eu/system/files/2022-10/methodology_to_assess_value_for_money_in_the_unit-linked_market.pdf.

7 See https://www.eiopa.europa.eu/system/files/2023-12/Consultation%20Paper%20on%20Methodology%20of%20Value%20for%20Money%20Benchmarks_0.pdf.